We’ve been very busy during the last 6 weeks writing Affordable Health Care (ACA) policies. Several of our customers had to wait until national enrollment to secure their new coverage and since they were customers of ours already, we were able to help. The premiums shocked most everyone I talked to and for those that couldn’t afford the increased costs, we were able to lower benefits to help them meet their premium needs for their budget.

The New York Times published an eye-opening article this past Tuesday that explains what we have been seeing. Securing new coverage is the beginning of even more expenses for each insured based on what their needs for coverage claims are. As you will see in this report, hardships arise even if the coverage is there.

////////////////////////////////////////////////////////////////////////

Here is the surest way to enjoy the peace of mind that comes with having health insurance: Don’t get sick.

The number of uninsured Americans has fallen by an estimated 15 million since 2013, thanks largely to the Affordable Care Act. But a new survey, the first detailed study of Americans struggling with medical bills, shows that insurance often fails as a safety net. Health plans often require hundreds or thousands of dollars in out-of-pocket payments – sums that can create a cascade of financial troubles for the many households living paycheck to paycheck.

Carrie Cota learned the hard way that health insurance does not guarantee financial security. Ms. Cota, a 56-year-old travel agent from Rosamond, Calif., learned she had the autoimmune disease lupus in 2007. She ran up thousands of dollars in medical and dental bills and ended up losing her job, and eventually her house.

“I had to move in temporarily with my ex-husband,” she said in a recent interview. “I’m staying with him until I can figure out what to do.”

In the new poll, conducted by The New York Times and the Kaiser Family Foundation, roughly 20 percent of people under age 65 with health insurance nonetheless reported having problems paying their medical bills over the last year. By comparison, 53 percent of people without insurance said the same.

These financial vulnerabilities reflect the high costs of health care in the United States, the most expensive place in the world to get sick. They also highlight a substantial shift in the nature of health insurance. Since the late 1990s, insurance plans have begun asking their customers to pay an increasingly greater share of their bills out of pocket though rising deductibles and co-payments. The Affordable Care Act, signed by President Obama in 2010, protected many Americans from very high health costs by requiring insurance plans to be more comprehensive, but at the same time it allowed or even encouraged increases in deductibles.

“We’re at a point where there’s been slow growth in health care costs and huge improvements in the numbers of people who have health insurance,” said Sara Collins, a vice president at the Commonwealth Fund, a health research group. “But there is this underlying trend towards higher cost sharing that could put increasing numbers of people at risk for being underinsured.”

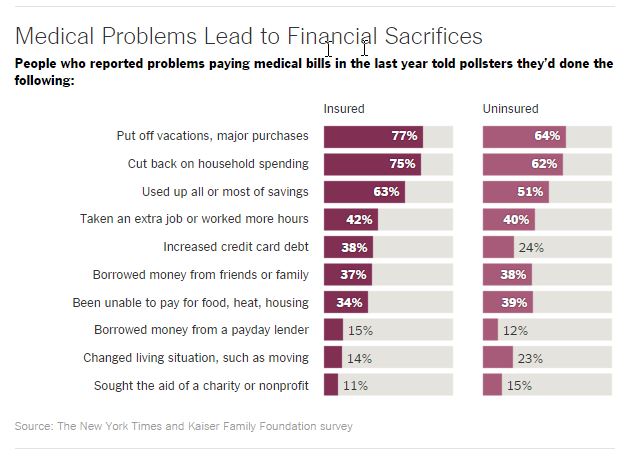

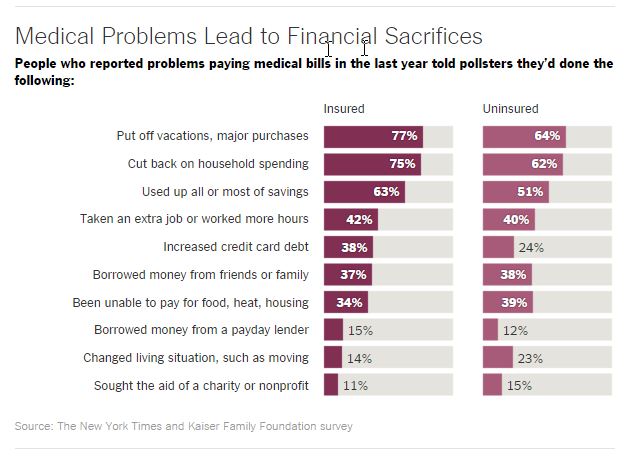

Among those who reported having problems paying their bills despite having insurance, 63 percent said they used up all or most of their savings; 42 percent took on an extra job or more work hours; 14 percent moved or took in roommates; and 11 percent turned to charity.

Randy Farris, 58, a factory worker from Conger, Minn., needed a knee replacement three years ago. His insurance covered 80 percent of the bill, but he needed to cash in an I.R.A. to pay his $4,000 share. “I haven’t been to the doctor since because I don’t want any more doctor bills,” he said. His wife’s retirement savings had been wiped out years before, he said, when he used them to pay her hospital bills after she died of cancer.

The health law has led to a decline in the number of Americans suffering financial stress from health problems, thanks to the new options for receiving coverage, especially for the poor. But the problem is still widespread, touching roughly a quarter of Americans under 65, when the insured and uninsured are looked at together. Americans older than 65 are covered by Medicare, which more frequently protects people from major financial trouble.

Unlike other polls, which have focused on the ways that insurance affects health care, the new Times-Kaiser survey explored the effects of medical bills on people’s daily lives well beyond the medical system. We found that medical bills don’t just keep people from filling prescriptions and scheduling doctors’ visits. They can also prompt deep financial and personal sacrifices, affecting their housing, employment, credit and daily lives. Kaiser has released a report today, detailing the survey’s main findings about this population.

“The major impact is actually a pocketbook or economic impact: their ability to pay the rent or the mortgage or buy food,” said Drew Altman, president of the Kaiser Family Foundation.

People without health insurance, of course, are more vulnerable to medical bills than those with health coverage. The study found that the people most likely to report bill problems were uninsured, poor or disabled. But the majority of people struggling with bills are insured. Of the people in the survey reporting difficulty with their medical bills, 34 percent lacked health insurance, 39 percent had insurance through work, 14 percent were covered through public programs and 7 percent had purchased their own health plans.

One reason, many experts said, is a gradual shift in the norms about the generosity of health insurance. In recent years, health plans have come with growing deductibles and narrowing networks of providers, provisions devised to lower the cost of premiums. Those features have made health insurance accessible to a larger share of the population, but may also be leaving more insured Americans vulnerable.

Ten years ago, David Dranove, a professor of health management at Northwestern’s Kellogg School of Management, conducted research on people experiencing medical bankruptcies. The study he co-authored found that bankruptcy was largely a problem of the uninsured. “But with more people buying less generous health insurance, I think the old evidence might no longer be relevant,” he said.

Insured people with financial problems often have plans with higher deductibles. But many said that the smaller co-payments piled up to make their care unaffordable. Many also received big bills that were not covered by their insurance. Among the 32 percent of insured patients stuck with an out-of-network bill, more than than two-thirds of patients said they didn’t know the provider wasn’t covered. More than 25 percent of the insured respondents said a medical claim had been denied.

Medical bill problems rarely occur in a vacuum, the survey found. Most of the people surveyed said their finances were tight even before there was an illness in their family. This pattern held true even for families higher on the income scale. The rates at which people with medical bill problems sought charity or borrowed money from friends was similar among people earning less than $25,000 and those earning more than $100,000.

Medical bill problems rarely occur in a vacuum, the survey found. Most of the people surveyed said their finances were tight even before there was an illness in their family. This pattern held true even for families higher on the income scale. The rates at which people with medical bill problems sought charity or borrowed money from friends was similar among people earning less than $25,000 and those earning more than $100,000.Research on medical bankruptcies has been controversial because it can be hard to untangle how medical bills fit into a family’s overall pattern of financial troubles. Twenty-nine percent of the people with medical bill problems said a family member had been forced to stop working or cut back on hours. (On the other side, about 41 percent of people said they’d taken on extra work to help pay bills.)

“Is that a job problem or a medical bill problem?” said David Himmelstein, a professor of public health at the City University of New York’s Hunter College School of Public Health who has studied medical bankruptcies. “It’s both of those things.”

The survey included a random sample of 1,204 adults under 65 who reported problems paying household medical bills in the past 12 months. Interviews were conducted online and by telephone between Aug. 28 and Sept. 28, and some respondents gave follow-up interviews in December. The margin of sampling error is plus or minus 4 percentage points. Information about the poll methodology is available here.

The survey asked people to describe the ways that bills had changed their lives. The chart above shows some of the most common answers.

If we can help you with any insurance needs you may have, please let us know. Our staff is readily available at 615.377.1212 or you can EMAIL us at info@BentonWhite.com. Visit our website too – there is loads of great information there at BentonWhite.com. We’re always ready to earn your business!

[Portions of this blog is taken from “Even Insured Can Face Crushing Medical Debt, Study Finds” by David Leonhardt, The New York Times / January 5th, 2016]